Paying off debt is like a long, uphill climb…a very long uphill climb!

One wrong step can make you tumble down. You need to make sure that you are doing things the right way. Today, we’ll talk about 5 mistakes that people make when paying off debt. That way you can avoid these problems in your own debt-free journey.

Let’s take a look at debt reconciliation done right!

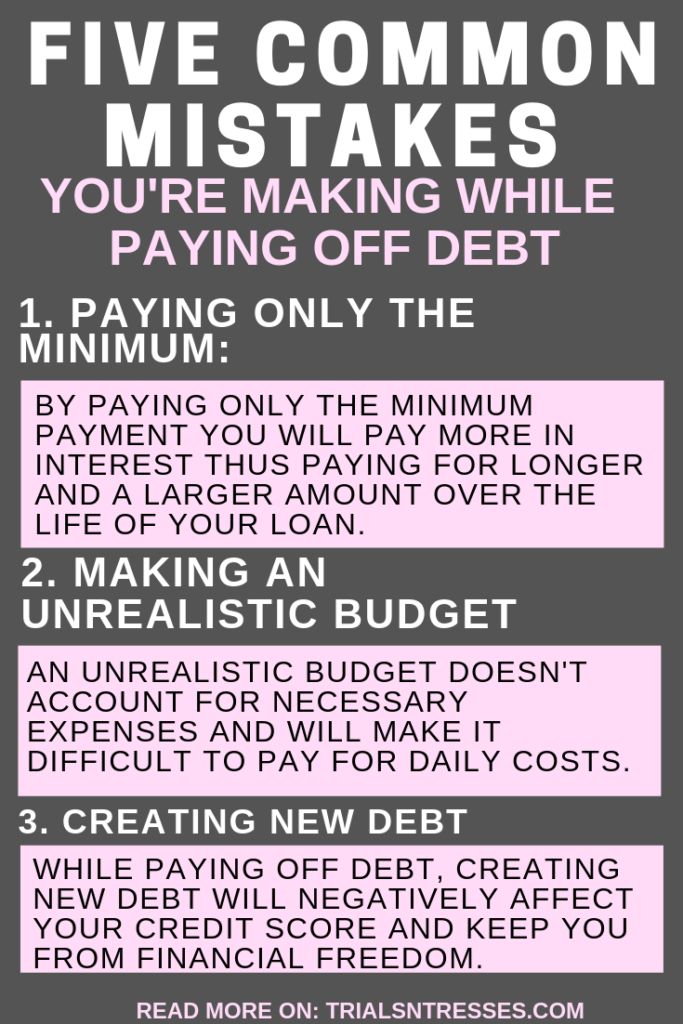

Failing to create a proper budget

When are paying off your debts, you are going to need to “cut corners” or slash your spending habits.

Sometimes you can get close to paying something off and the temptation hits you to pay it off right away – causing you to be late on rent, utilities, or your car payment. Whoops!

It’s not fun, but you are going to need to anticipate how much you need to spend to get by while you are paying out additional funds to settle your debt. This will help to ensure that you don’t find yourself worse off than before, just because you decided to start paying off your debts!

If you’re going to do this, do it right—make a budget and stick to it—read even more from Fortune.

Closing accounts after you’ve paid them off

Some people pay off a credit debt and immediately close out that account, thinking “good riddance!” This is a mistake. Your credit rating is going to be based on lots of different factors. One of them is how much available credit you have.

So, when you pay off those accounts:

1. Keep them open.

2.Make a small purchase now and then.

3.Pay it off on time and in full.

This will build your credit up much faster because it will look like you have lots of credit available. But you are controlling yourself and not abusing the privilege.

Trying to pay off too many debts at once

If you have a lot of debt, you want to give a focused approach to paying it off. Paying a small amount to everyone is not the way to go. Find out which credit card has the highest interest rate and put your focus on this one until you pay it off.

If you don’t, those high interest rates are very costly over time, so focused on the most expensive debt first.

After you pay that off, go to the debt with the highest interest rate on the list and repeat the process. Don’t worry, you’ll get there, and the money that you save knocking out the highest-interest debts will serve you well and get you out of debt faster.

Stopping retirement payments while paying off debt

If you’ve got a 401(k) or another form of retirement plan, paying off your debts is not a good reason to neglect to put money in your retirement.

It’s an easy mistake to make, after all, since you won’t be using those funds for another 10, 20, or even 30 years. But, regardless, this is a mistake.

Keep putting at least 5% to 10% of your income into retirement so that you don’t suffer in the long run. Aside from the long-term benefits, some 401(k) plans also offer low-interest loans that you can take out in emergencies.

So, keeping at least some minimal cash flow going into that retirement account is a very, very good idea that gives you a lot of options.

https://believeinabudget.com/12-mistakes-i-made-while-paying-off-debt/

Not checking your credit report

One of the most common mistakes that people make when they are paying off debt is a failure to check their credit reports. The 3 reporting agencies:

1.Experian,

2.Equifax, and

3.TransUnion

Each one is required by law to give you a free credit report every year, but you have to contact them and request it.

Having a copy of your credit report is vital. It allows you to check for inaccuracies, and, if you find them, you can ‘challenge’ these debts—read more from the Confused Millennial. After you challenge these debts, if the debtor does not prove that you owe them within a certain time, they must be taken off your credit report.

To get the most out of this, request a copy of your credit report from one agency at a time, every 4 months.

So, for instance:

You request a copy of your credit report from Experian in January,

Then, in May you request one from Equifax,

And, in September you get one from TransUnion.

This will give you an ‘ongoing view’ of your credit score throughout the year that is much more useful than getting them all in one shot.

Some final words

Today we’ve talked about 5 mistakes people make paying off debt and as you can see, there are a lot of pitfalls out there that you might not be expecting. By using our tips, you can avoid them, just start by making yourself a budget. Keeping accounts open as you pay them to make your credit look more attractive.

Don’t put too much on your plate by trying to pay off too many debts at once and definitely don’t stop paying into your retirement. You’re gonna need that someday and it gives you options. Finally, take advantage of your yearly free credit reports so that you can track your progress and challenge any mistakes that you find.

Hang in there. While it’s a long, uphill road, these tips and your determination will pay off.

To read more on topics like this, check out the Money category

Leave a Reply